New accounting rules coming in 2019 will affect your ability as a business owner to get a business loan and attract investors, as well as how much business tax you pay.

Part 1 of 3

Part 2: 4 Steps to Preparing for New Accounting Rules on Commercial Real Estate Leases

Part 3: 5 Ways to Protect Your Commercial Real Estate Lease in a New Accounting Climate

Here are the five things that tenants of commercial real estate need to know about the proposed new accounting rules that affect how leases are reported in financial statements.

1. What’s changing?

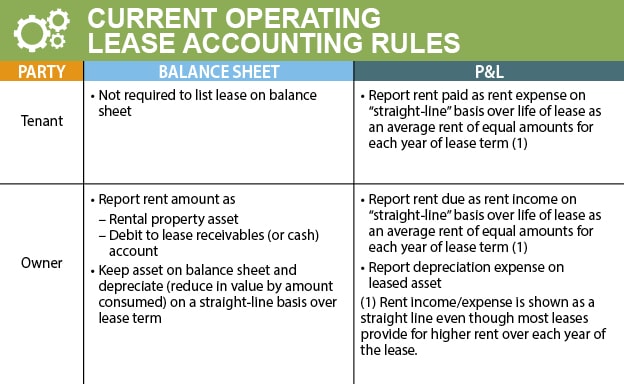

Accounting rules require companies to keep two basic financial statements.

- A balance sheet lists assets and liabilities showing what the company owns and owes. Recorded assets equal, or “balance,” recorded liabilities plus equity.

- An income statement (also called P&L) lists the company’s revenues and expenses. This makes it possible to calculate the company’s profits and losses.

The new accounting rules would eliminate the rule that tenants don’t have to list operating leases on their balance sheet.

Once imposed, the rule will require that all leases be shown on the balance sheet.

The change is to ensure that investors, banks, regulators and other stakeholders in the financial system get the information they need to make sound judgments about a company’s financial condition.

The Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB), which set accounting rules, felt that letting tenants keep operating leases off their balance sheets was creating too big a blind spot in the financial system.

2. How does this affect me?

2. How does this affect me?

Financial statements affect a company’s ability to attract investors and get bank loans and how much it pays in taxes.

When you no longer can keep leases off your balance sheet, your total lease payment obligations over the course of the lease must be recorded as an up-front liability at the start of the lease.

Adding a massive new liability of six to eight figures to the balance sheet each time you enter into a lease may do at least some harm to your company’s financial position.

The more leases you make, the more your financial statements and ratios will suffer. It will be harder to attract new investment and loans. The added liabilities may even cause you to default on your current loans.

3. What are the current accounting rules for leases?

If you have an operating lease, your landlord gives you, as the tenant, a right to use land or another asset. You don’t own the asset and must return it to the landlord after the lease ends. Most standard commercial real estate leases are operating leases.

In a capital lease, you purchase an ownership interest in the leased asset.

The crucial accounting difference between the two kinds of leases is that tenants aren’t required to record operating leases on their balance sheets.

4. Why should I care about this now?

FASB and IASB are working on the rules, which are contained in the 343-page “Revised Exposure Draft” published on May 16, 2013. The rules are expected to take effect as early as Jan. 1, 2019 for public companies and Jan. 1, 2020 for private companies.

The rules will require that you look at and revise financial statements that you’re generating now.

- There’ll be no grandfathering of existing leases. All leases will have to be accounted for in accordance with the new rules on the effective date no matter when they were signed or took effect. Owners and tenants will have to revise their balance sheet and P&L before the rules actually take effect so they comply on day one.

- Financial statement revisions may be necessary. If your company is required to provide a three-year comparison in its financial statements, you’ll have to revise your 2015 and 2016 financial statements once the final rules come out.

5. What’s my first step?

In our next article, we’ll discuss what you need to do to prepare for the new accounting rules regarding commercial real estate leases. We’ll offer some strategies to best position your finances.

In the meantime, we suggest you consult your account, tax consultant or tenant representative for advice.

Share your experiences on working with Commercial Real Estate Group of Tucson.